US Dollar Fundamental Forecast Talking Points:

- This past week, US inflation cooled further, the Fed hiked 50bps while raising its terminal rate forecast and economic activity measured by the PMI sunk deeper into negative territory

- Out of the fundamental mix, the Dollar struggled to find a clear direction; which may reinforce expectations for holiday conditions ahead

- However, thin liquidity can readily transmit unexpected volatility ahead with event risk like the PCE deflator, consumer confidence and housing data ahead

Recommended by John Kicklighter

Traits of Successful Traders

Fundamental Forecast for the US Dollar: Neutral

There are a few competing fundamental themes working on the US Dollar at the moment. Between interest rate speculation and the currency’s safe haven role, we have seen bearish pressure level out to uncertainty for the market this past week. These will absolutely be the top matters to watch moving forward, but it is also important to have a perspective of the general market environment through the next few weeks to gain a better appreciation for how the currency (and other assets) will interact with fundamentals as they hit the tape. Historically, the final two weeks of the year typically see a significant drop off in liquidity (volume and open interest) as the last salvo of major global event risk and policy decisions are usually cleared. It is possible to reverse this norm, but it is very unusual; and generally, it tends to occur when there is a charged sense of ‘fear’. If the markets do quiet, it will likely work against the development of trends – in both fundamental views and price action. That said, thinner markets can also lead to more dramatic swings in volatility as surprises have less market depth to absorb shock.

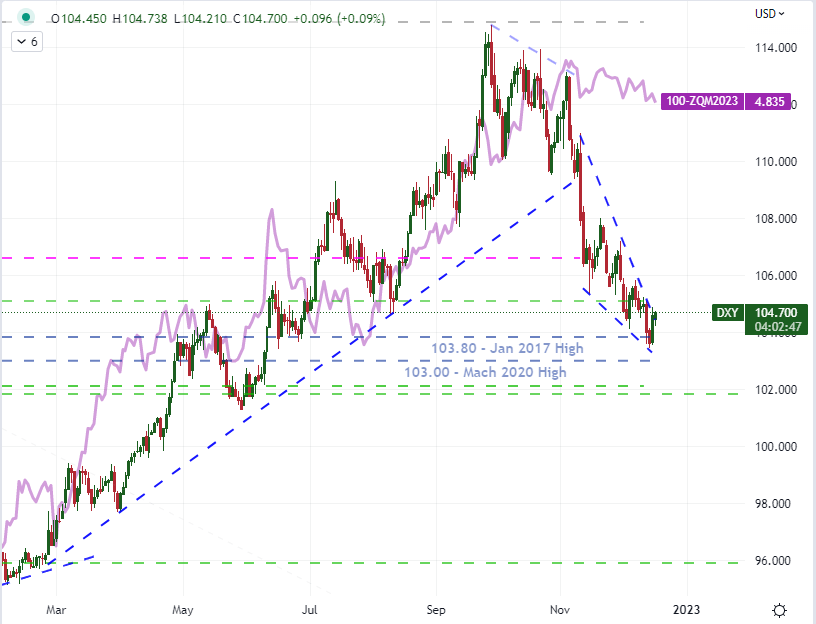

Whether or not full-fledged trends that can carry over into 2023 develop over the coming week requires a watchful eye. On the other hand, even protracted volatility from the Dollar and the majors could generate some noteworthy technical breaks. The DXY Dollar Index has worked its way into a very prominent descending wedge which is like essentially throwing the breaks on what was a very prominent bull trend breakdown back in early November. The charge behind that move seems to directly link to the October CPI release, which notably capped 2023 interest rate expectations. Ever since that peak, we have seen the market and Fed live at odds over what the monetary policy path would be for the coming year. The FOMC decision made it clear that they believe the benchmark rate will rise to 5.1 percent (the median) and stay there through the entire year. Fed Funds futures on the other hand are unrelating in calling for a peak around 4.80-90 percent and then pricing in two rate cuts in the second half of the year. This will be a battle ground for the Dollar going forward. The question is whether we can see any progress on it this week.

Chart of DXY Dollar Index Overlaid with the Fed Funds Futures Forecast for June 2023 (Daily)

Chart Created on Tradingview Platform

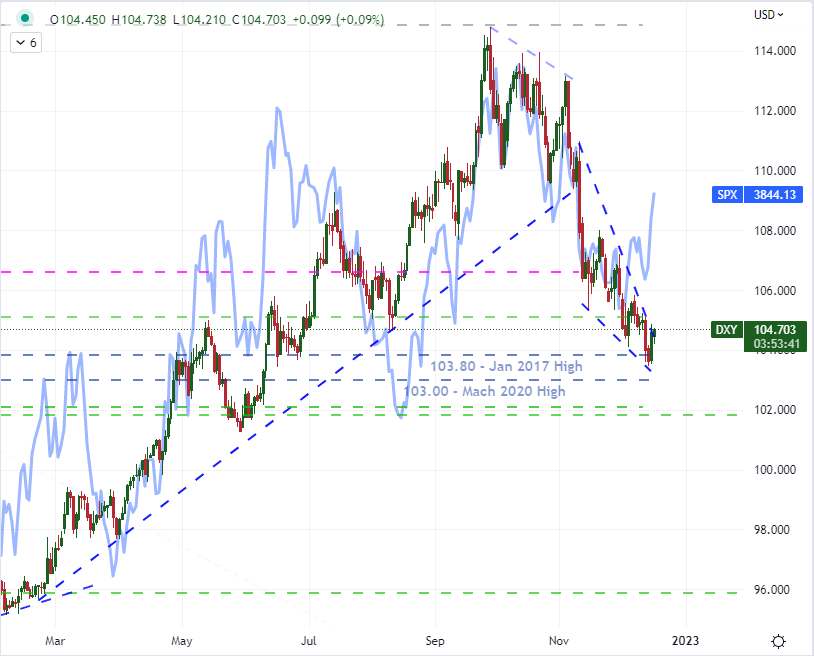

The other major fundamental theme that I will be monitoring closely through the coming week is the ebb and flow of risk trends. The correlation between the DXY and the S&P 500 is particularly strong and ‘negative’ – meaning they tend to move together but in opposite directions. This caters to the Greenback’s role as a safe haven asset based largely in its place as the most liquid currency backing the largest economy in the world. Notably, this relationship has waned somewhat over the past week. As the US equity market dove following the failed breakout after the CPI release, the Dollar’s own reaction was more restrained. Here is where liquidity will be more important. Should holiday conditions kick in, it will likely throttle the S&P 500’s progress to new lows, which will in turn cap the Dollar’s safe haven bid. That said, there is still an opportunity for the currency to close the gap it has recently opened up in its relationship.

Chart of DXY Dollar Index (Daily)

Chart Created on Tradingview Platform

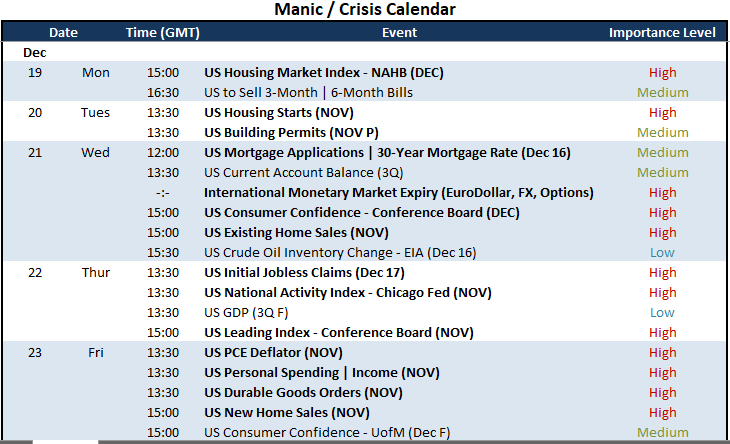

For catalysts to either of these core fundamental themes, it would be wise to look to the economic docket. ‘Sentiment’ can be amorphous and can turn and accelerate without provocation. However, waiting for the unknown is not an approach I usually take to the markets. In contrast, the economic calendar is conveniently demarked with dates and times as well as a good guideline as to what can tap a stronger fundamental theme behind the market’s ebb and flow. For the most provocative event, there is a very inconvenient release time on Friday when we are almost into the Christmas weekend. The PCE deflator is the Fed’s favorite inflation reading, so it carries a lot of weight. That said, it is unlikely to redefine the market’s view just before the weekend – or we won’t realize that adjustment until liquidity is restored. Instead, I will be looking for Fed commentary as more timely provocation on this front. Otherwise, recession concerns will also be something to measure in the data run. We have the Conference Board’s consumer confidence survey on tap Wednesday, but the run of housing data through the week will give another broad sector insight.

Top US Macro Event Risk Next Week

Calendar Created by John Kicklighter

Discover what kind of forex trader you are